Service-sector SMEs challenges and the way out

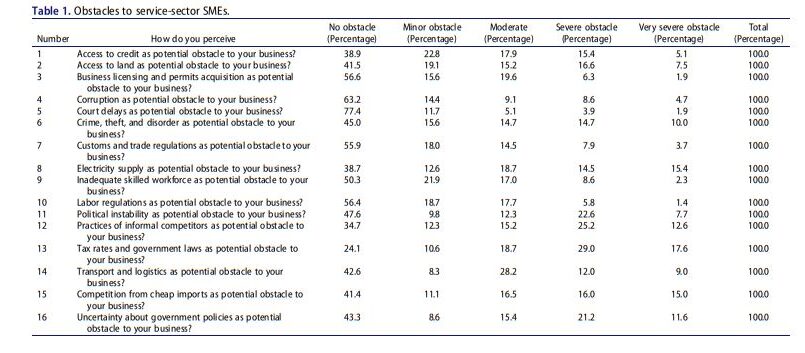

For the quantitative aspect of the study, participants were given a list of 16 obstacles that SMEs face and asked to select their perceived level of severity of the obstacles to their businesses on a five-point Likert scale from no obstacle to very severe obstacle. The obstacles and the level of severity are listed in Table 1. The researchers then combined the percentage of participants who selected severe obstacle and very severe obstacle for each item and ranked the obstacles in Table 2 to determine how the obstacles had been rated by SMEs and the implications thereon. From Table 2, the highest-rated obstacle was tax rates and government laws with 46.65 percent of participants perceiving this as the biggest challenge to their businesses. Practices of informal competitors was the second most rated obstacle, perceived by 37 percent of the participants as either a severe or very severe obstacle to their business. Uncertainty about government policies and competition from cheap imports were ranked third and fourth respectively. Political instability due to changes in government and electricity were fifth and sixth, while crime, theft, and disorder and access to land followed. Access to finance was ranked 10th. Court delays (5.78 percent), followed by labor regulations (7.18 percent) and business licenses and permits (8.23 percent) were the least rated perceived obstacle to service-sector SMEs. The suggested solutions to the challenges by the participants as outlined in a word cloud in Figure 1 includes government’s reduction in taxes, consistent policies, control of the importation of inferior goods, government to deal with the inflation rate, stability of the Cedi, access to cheap sources of funds, ability to market goods and services, the need for trained personnel, and ensuring regular power supply, among others.

Implications for theory and practice

Governments and institutions are making an effort to ensure there is financial inclusion of businesses and individuals through innovative approaches (Senyo & Osabutey, 2020), the availability of credit to SMEs (Lu et al., 2020), and development of entrepreneurship ecosystems as a mechanism to enhance development in the wake of a global health pandemic (Liguori & Bendickson, 2020). This study has helped to identify the challenges faced by service-sector SMEs. The implication is that policies and solutions to SMEs’ challenges should be tackled from the top down according to the rankings of the challenges identified in this study. Figure 2 outlines the challenges and solutions of service-sector SMEs from both FIs’ and SMEs’ point of view and provides implications if tackled by the responsible institutions. For service-sector SMEs to be sustainable and continue to be the engines of economic growth, it is recommended that government and other stakeholders use the challenges identified and the solutions as part of their development of the service-sector SMEs. This will have diverse implications on ease of doing business, growth of SMEs, improved access to funding, and growth in the GDP.

References

Abor, J., & N. Biekpe. (2006). Small business financing initiatives in Ghana. Problems and Perspectives in Management, 4(3), 69–77. https://www.researchgate.net/profile/Nicholas[1]Biekpe/publication/265484299_Small_Business_Financing_Initiatives_in_Ghana_1/links/ 54e6f2990cf277664ff760a2/Small-Business-Financing-Initiatives-in-Ghana-1.pdf

Abor, J., & P. Quartey. (2010a). Issues in SME development in Ghana and South Africa. International Research Journal of Finance and Economics, 39(January), 218–228. https:// www.smallbusinessinstitute.co.za/wp-content/uploads/2019/12/ IssuesinSMEdevelopmentinGhanaandSA.pd f

Abor, J., & P. Quartey. (2010b). Issues in SME development in Ghana and South Africa. International Research Journal of Finance and Economics, 39(39), 218–228. Asare, A. O. (2014). Challenges affecting SME’s growth in Ghana.

Asare/OIDA International Journal of Sustainable Development, 7(6), 23–28. http://www.ssrn.com/link/OIDA

Ayandibu, A. O., & J. Houghton. (2017). The role of small and medium scale enterprise in local economic development (LED). Journal of Business and Retail Management Research, 11(2), 133–139. https://www.proquest.com/scholarly-journals/external-forces-affecting-small-busi nesses-south/docview/2028982053/se-2?accountid=14648

Ayyagari, M., V. Maksimovic, & A. Demirgüç-Kunt. (2017, November 14). SME finance. World Bank Policy Research Working Paper No. 8241. SSRN.

Bauweraerts, J., C. Pongelli, S. Sciascia, P. Mazzola, & A. Minichilli. (2021). Transforming entrepreneurial orientation into performance in family SMEs: Are nonfamily CEOs better than family CEOs? Journal of Small Business Management, 1–32. https://doi.org/10.1080/ 00472778.2020.1866763

Beck, T., & A. Demirgüç-kunt. (2008). Access to finance : An unfinished Agenda. The World Bank Economic Review, 22(3), 383–396. https://doi.org/10.1093/wber/lhn021

Brixiová, Z., T. Kangoye, & T. U. Yogo. (2020). Access to finance among small and medium[1]sized enterprises and job creation in Africa. Structural Change and Economic Dynamics, 55 (December): pp 177–189 .

Calabrese, R., M. Degl’Innocenti, & S. Zhou. (2020). Expectations of access to debt finance for SMEs in times of uncertainty. Journal of Small Business Management, 1–28. https://doi.org/ 10.1080/00472778.2020.1756309

Demartini, M. C., & V. Beretta. (2020). Intellectual capital and SMEs’ performance: A structured literature review. Journal of Small Business Management, 58(2), 288–332. https://doi.org/10.1080/00472778.2019.1659680

Donbesuur, F., G. O. A. Ampong, D. Owusu-Yirenkyi, & I. Chu. (2020). Technological innovation, organizational innovation and international performance of SMEs: The moderating role of domestic institutional environment. Technological Forecasting and Social Change, 161(February), 120252. https://doi.org/10.1016/j.techfore.2020.120252

Liguori, E., & J. S. Bendickson. (2020). Rising to the challenge: Entrepreneurship ecosystems and SDG success. Journal of the International Council for Small Business, 1(3–4), 118–125. https://doi.org/10.1080/26437015.2020.1827900

Lu, Z., J. Wu, & J. Liu. (2020). Bank concentration and SME financing availability: The impact of promotion of financial inclusion in China. International Journal of Bank Marketing, 38(6), 1329–1349. https://doi.org/10.1108/IJBM-01-2020-0007

Mabe, D. M. K., F. N. Mabe, & F. Y. N. Codjoe. (2013). Constraints facing new and existing small and medium-scale enterprises (SMES) in greater accra region of GHANA. International Journal of Economics, Finance and Management, 2(1), 160–168.

Mamman, A., J. Bawole, M. Agbebi, & A. R. Alhassan. (2019). SME policy formulation and implementation in Africa: Unpacking assumptions as opportunity for research direction. Journal of Business Research, 97(April), 304–315. https://doi.org/10.1016/j.jbusres.2018.01. 044

Masiello, B., & F. Izzo. (2019). Interpersonal social networks and internationalization of traditional SMEs. Journal of Small Business Management, 57(S2), 658–691. https://doi.org/ 10.1111/jsbm.12536

Nguyen, B. (2018). Entrepreneurial reinvestment: Local governance, ownership, and financing matter. Academy of Management Proceedings, 2018(1), 13097. https://doi.org/10.5465/ AMBPP.2018.13097abstract

Oppong, M., A. Owiredu, & R. Q. Churchill. (2014). Micro and small scale enterprises development in Ghana. European Journal of Accounting Auditing and Finance Research, 2 (6), 84–97. https://www.eajournals.org/wp-content/uploads/Micro-and-Small-Scale[1]Enterprises-Development-in-Ghana1.pdf

Quartey, P., E. Turkson, J. Y. Abor, & A. M. Iddrisu. (2017). Financing the growth of SMEs in Africa: What are the contraints to SME financing within ECOWAS? Review of Development Finance, 7(1), 18–28. https://doi.org/10.1016/j.rdf.2017.03.001

Radic, D. (2020). Small matters! Journal of the International Council for Small Business, 1(1), 24–27. https://doi.org/10.1080/26437015.2020.1714357

Rita, M. R., & A. D. Huruta. (2020). Financing access SME performance: A case study from batik SME in Indonesia. International Journal of Innovation, Creativity and Change,12(12), 203–224.

Seidel-Sterzik, H., S. McLaren, & E. Garnevska. (2018). Effective life cycle management in SMEs: Use of a sector-based approach to overcome barriers. Sustainability (Switzerland), 10 (2), 1–22. https://doi.org/10.3390/su10020359

Senyo, P. K., & E. L. C. Osabutey. (2020). Unearthing antecedents to financial inclusion through FinTech innovations. Technovation, 98, 102155. https://doi.org/10.1016/j.technova tion.2020.102155

The Ghana Statistical Service (GSS). (2018). The Integrated Business Establishment Survey (IBES): Comprehensive Sectoral Report [online]. Available from: https://www2.statsghana. gov.gh/docfiles/publications/IBES/IBES%20II%20COMPREHENSIVE%20SECTORAL% 20REPORT.pdf